Mortgages

How do I get a mortgage and pay it off?

This 9,500-word Epic Guide to Mortgages is the definitive article on how to get a mortgage and pay it off faster, today in 2026. The Ultimate Guide.

Mortgages

10 min read

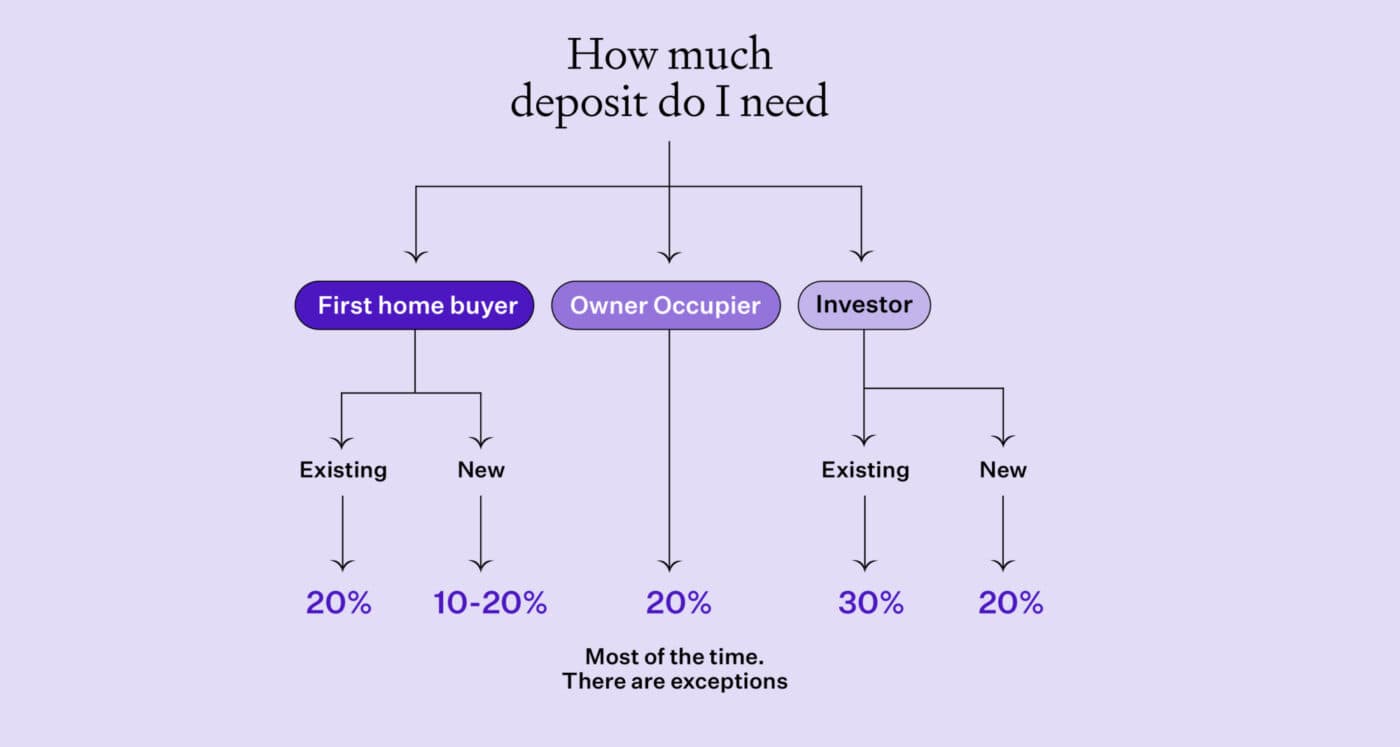

Most people think they know how much deposit they’ll need to buy a house.

But the deposit you need changes. It’s all because of the loan-to-value ratio (LVR) restrictions.

Under these rules, your deposit changes depending on:

LVRs, or Loan-to-Value Ratios, are rules set by the Reserve Bank to decide the minimum deposit you need to get a mortgage. For example, property investors usually need a 30% deposit for existing homes and 20% for new builds. Owner-occupiers generally need a 20% deposit. These rules help keep the financial system stable and can change depending on your situation.

In this article, you’ll learn what LVRs are and how they apply to you.

| Buyer type | Property type | Minimum deposit | Speed limits and exemptions |

| Owner-occupiers | Existing property | 20% | Up to 25% of each bank’s lending can be at a lower deposit. Kāinga Ora First Home Loans are exempt from LVR restrictions. |

| Property investor | Exisiting property | 30% | Up to 10% of each bank’s lending can be at a lower deposit. |

| Property investor | New Build | 20% | New Builds are exempt from the LVR restrictions. |

The Reserve Bank sets the LVR rules to limit low-deposit lending. This is to make the financial system safer.

In this article you’ll learn what LVRs are and how they impact how much deposit you need to buy a house.

Before we get started, it’s worth pointing out that the LVR restrictions will likely change by July 2024.

The Reserve Bank plans to bring in new mortgage rules called the Debt to Income ratios (DTIs). This will happen mid-2024.

Once those new rules are in place, the Reserve Bank will change the LVR rules.

Under the new rules, investors will only need a 30% deposit to buy an existing property, whereas they currently need a 35% deposit.

This will mean some property investors will be able to buy where they couldn’t before.

If you plan to invest in a New Build, everything stays the same. You still only need a 20% deposit.

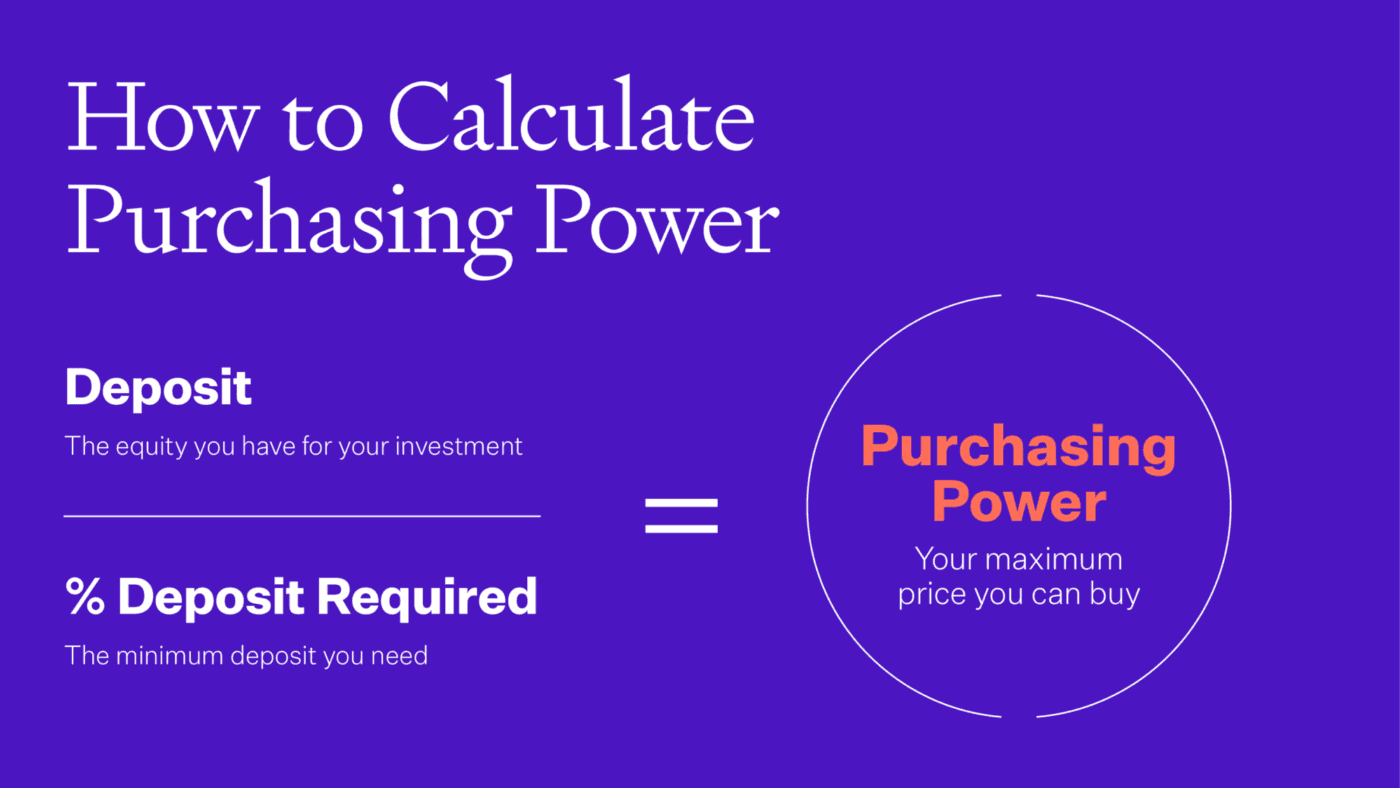

Loan to Value Ratio restrictions (LVRs) are the rules that say how much a bank can lend you.

It’s the percentage of your mortgage compared to the value of your property.

For instance, let’s say you want to buy your own home. The bank can lend you up to 80% of the money. That means you need to put in the rest. That’s your 20% deposit.

Here are the current LVR restrictions:

These rules are set by the Reserve Bank of New Zealand. That’s the part of the government that makes the rules for all commercial banks. Banks like ASB, BNZ, ANZ and Westpac.

To give another example, let’s say you’re an owner-occupier. You’re eyeing up a house that’s $1 million. The bank is only allowed to lend you up to 80%, so the 20% left over is the deposit you have to front.

If you’re looking to buy your own home, you need a 20% deposit. So, the formula is then:

$200,000 / 0.2 = $1,000,000 of purchasing power.

You can spend up to $1 million on a property.

That is made up of a $200,000 deposit and $800,000 worth of lending.

| Buyer type | Deposit required | Calculation | Maximum purchase price |

| Owner-occupier | 20% | $200,000 ÷ 0.20 | $1,000,000 |

| Investor buying an existing property | 30% | $200,000 ÷ 0.30 | $666,667 |

That is one of the main ways LVR rules affect buyers. Even with the same deposit, investors are often limited to a lower purchase price than owner-occupiers.

Use our LVR calculator to work out your deposit requirement and potential maximum purchase price.

In this example, both the owner-occupier and the investor have the same $200,000 deposit.

But, the owner-occupier can borrow more than the investor.

That disadvantages investors compared to owner-occupiers. Some Kiwis would say that’s not a bad thing.

Use our LVR calculator to find out the LVR of your property:

You might think the LVR restrictions have a big impact on the property market.

That’s not really the case, especially when property prices are rising fast.

As property prices rise, borrower’s loans get smaller compared to the property’s value. So your LVR goes down.

So, as house prices rise, property owners can borrow more anyway.

That’s partly why when LVRs came back in (2021), they had little impact on house price inflation.

Let’s look at some examples of how LVR restrictions can impact individual buyers.

Jenny is a first home buyer. She and her partner, Steve, saved a $70,000 deposit.

Without any LVR restriction, Jenny and Steve might secure a 10% deposit home loan.

That would mean the couple can buy a property worth $700,000.

That’s enough to buy a nice 3-bedroom home in their home city of Christchurch.

But, if Jenny and Steve have to follow the 20% LVR rule, they can only buy a property worth $350,000.

That’s not enough to buy a home that suits their needs or tastes. So, Jenny and Steve can’t buy.

Buyers who can still buy these sorts of properties now have less competition.

This softens housing demand, and house price inflation slows.

If Jenny and Steve want to enter the market, they will need:

Jeremy bought his first property 2 years ago in Wellington. It’s a tiny shoebox apartment in the central city. But, despite its limited market, the property has gone up in value gradually each year.

Now, Jeremy and his partner plan to adopt. So, the couple want a larger home to provide for their growing family.

He plans to sell his apartment and use the money as a deposit for his next home.

After selling the property and paying the real estate agent, he’ll be left with $150,000.

So he starts looking at properties in the $725,000 - $750,000 range.

Under the LVR restrictions, Jeremy’s $150,000 deposit will be enough to secure a mortgage of up to $600,000.

So Jeremy can spend up to $750,000 on a property.

While Jeremy can still afford a home in his price range, he is limited in how much he can compete with other buyers.

He can’t bid up the prices as much. This decreases competition, dampening house prices.

Lastly, let’s look at Barbara and Bruce. This couple “buy and flip” properties, doing them up to sell at a profit.

They’ve been in the game for a while and prefer to use a large deposit while renovating each property. This helps lower interest costs.

They’re looking in the same price range as Jeremy (from our last example), i.e. in the $725,000 - $750,000 range.

But, because they have a $350,000 deposit, they have no concerns about the LVR restrictions.

With a $350,000 deposit, Barbara and Bruce have a purchasing power of $1,000,000.

The couple don’t want to spend that much. But, if they have to pay $770,000 for a house that is “worth” $750,000, they’ll do it. They can easily outbid Jeremy.

The LVR restrictions do not impact Barbara and Bruce.

There are several exemptions to the LVR rules where low deposit loans are still possible:

| Year | What changed |

| 2013 | LVR restrictions introduced |

| 2015 | Auckland investor deposit set at 30% |

| 2016 | Investor deposit increased to 40% nationwide |

| 2018 | Investor deposit reduced to 35% |

| 2019 | Investor deposit reduced to 30% |

| 2020 | LVR restrictions removed during Covid |

| 2021 | LVRs reintroduced. Initially the investor deposit was 30%, then lifted to 40% |

| 2023 | Investor deposit reduced to 35% |

| 2024 | Investor deposit reduced to 30% |

The biggest exclusion is for New Builds. No LVR restrictions apply. It’s up to the banks how much they’ll lend to you.

This applies to homeowners and investors, but it matters more for investors.

In practice, you can buy an investment property using a 20% deposit rather than a 35% deposit.

Take the example of two $700,000 properties standing side by side. One is existing, and one is a New Build.

If an investor buys the existing property, they require $245,000 as a deposit. But, if they decide to purchase the brand new property, they’ll only need a $140,000 deposit.

This exemption makes New Build properties more attractive to investors. That encourages developers to build more houses.

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser