Mortgages

Interest only mortgage calculator & guide to interest only mortgages NZ

Discover if an interest-only loan could lower your payments and boost your properties cash flow.

Mortgages

2 min read

Here is your monthly interest rate report. The main points:

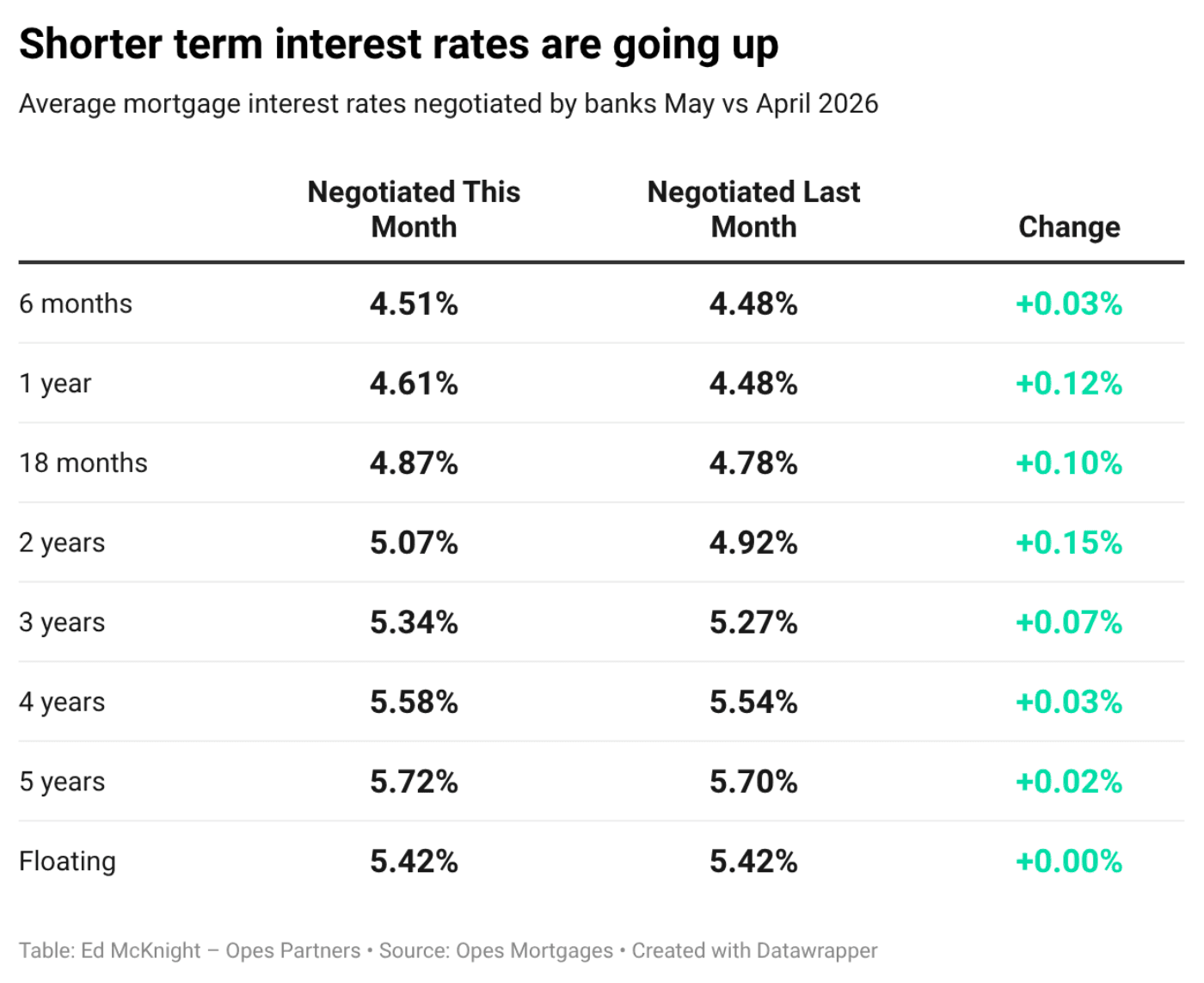

If I look at the report I sent last month, the 3-5 year rates were moving up. This month, the shorter-term rates are nudging up.

The average 1-year negotiated rate moved from 4.48% to 4.61%.

The 2-year rate moved even more. That’s up 0.15% to 5.07% on average.

The longer-term rates barely moved this month.

So if last month was about long-term rates rising, this month is about shorter-term rates catching up.

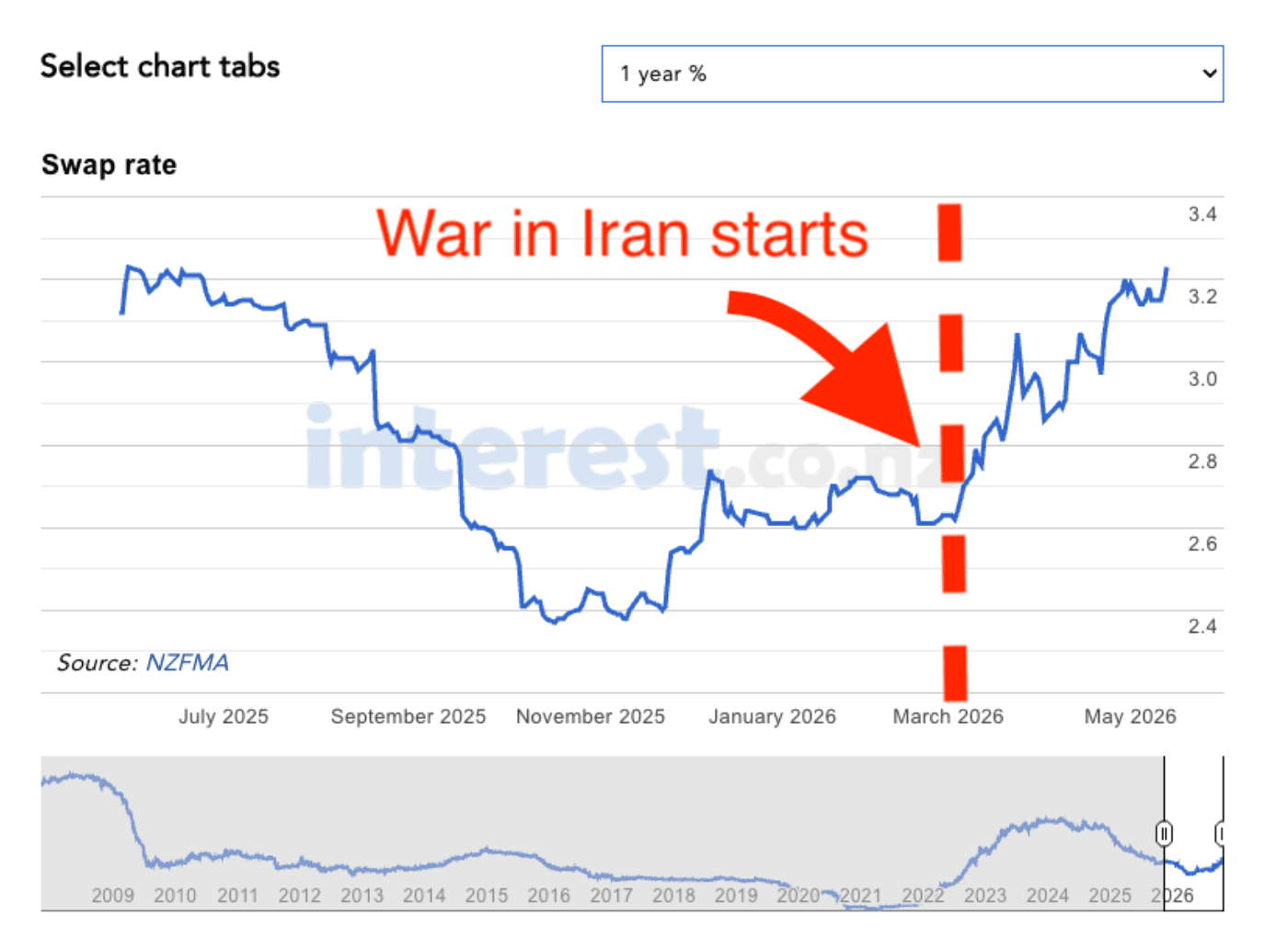

Swap rates have shot up. Think of these as what it costs the bank to borrow and then lend money to you and me.

The 1-year rates have shot up since the start of the year and the start of the Iran war.

What's driving the swaps? Two things.

First, oil prices. The Iran war is pushing up oil prices. That’s making people worry about spillover inflation. Since almost everything you buy needs oil to get on the shelf.

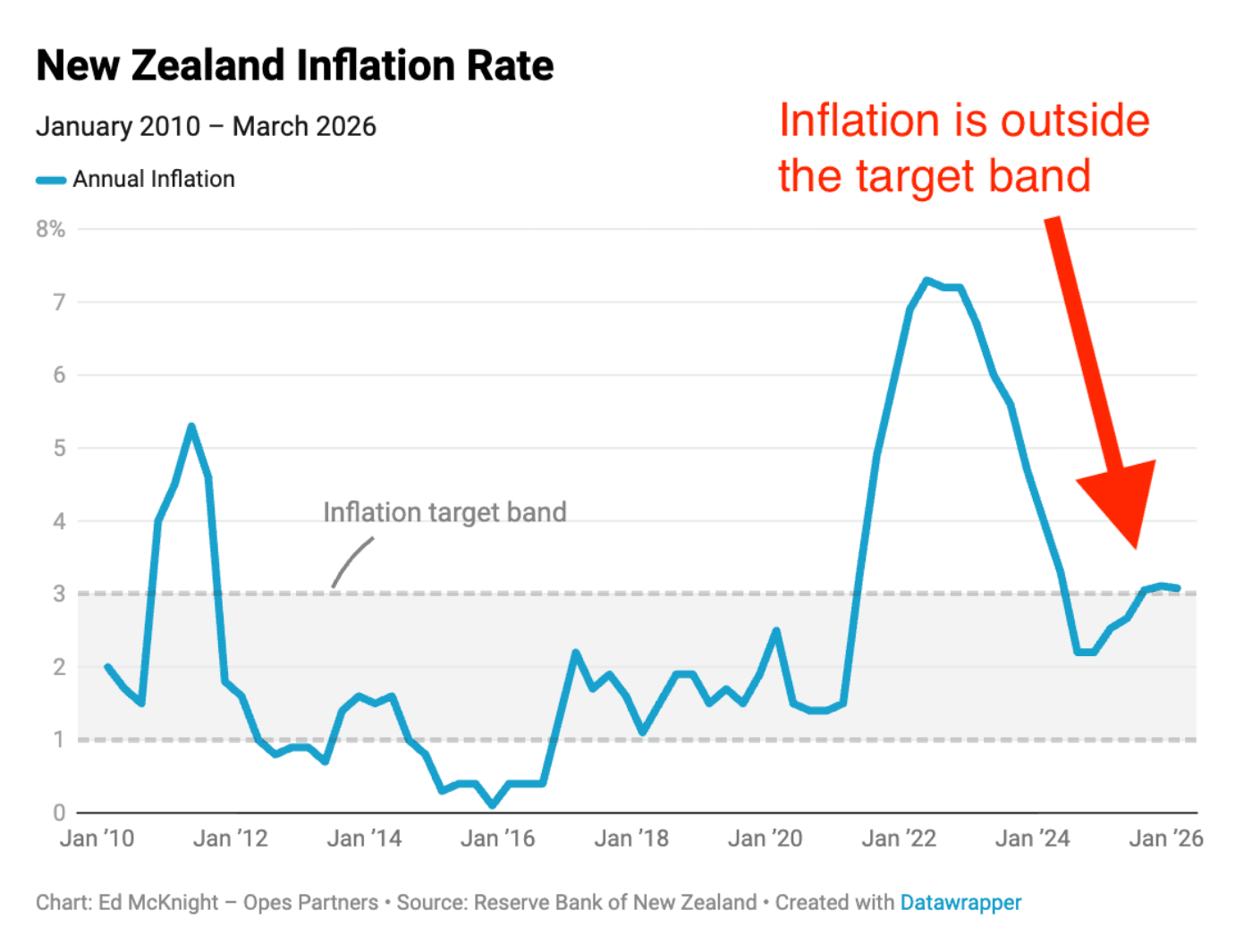

Second, and this is the more important one, inflation has come in higher than the Reserve Bank was forecasting.

Inflation came in at 3.1%. That’s compared to the Reserve Bank’s forecast of 2.8%.

That’s why banks think that the OCR could go up faster than they previously thought.

ANZ is most worried. Its economists now expect three OCR increases in a row. They reckon the OCR is going to 3.00%.

But then you have Kiwibank on the other side. They think that the economy is still fragile and will need support.

So even the bank economists don't agree on where this is heading.

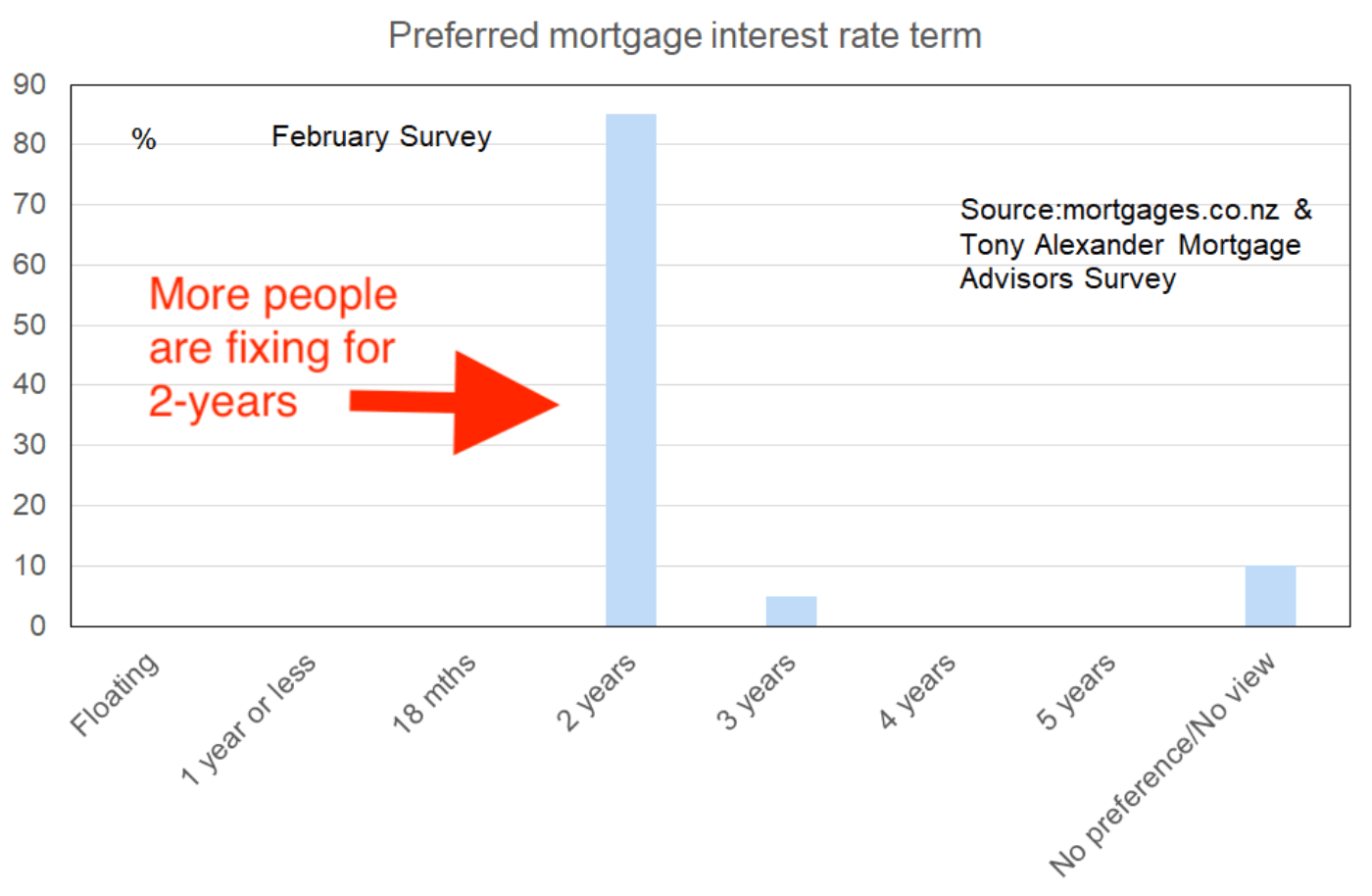

At Opes Mortgages, I’m seeing more investors choosing longer-term fixes.

A year ago, the one-year rate was the preferred option for most. Now investors are increasingly fixing for two years.

That's not just us. Tony Alexander's latest mortgage advisers survey found 85% of brokers say two years is the preferred term for borrowers right now.

Only 5% are seeing three years as preferred, and not many people are fixing for just a year.

This is a big shift. Through 2024 and most of 2025, one-year fixes were most popular. That’s because borrowers thought rates would come down. (They were right.)

But the interest rate that suits your situation depends on:

So it’s worth talking to a mortgage adviser to make the right decision for you.

If you've got a question about your mortgage, hit reply and I'll come right back to you.

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser