Property Investment

The next OCR change

The OCR didn’t move. But what the Reserve Bank said could shape your mortgage for the next two years. Here’s how👇

Property Investment

2 min read

Here is your monthly interest rate report.

This gives you a quick, plain English update on how much your mortgage costs.

What you need to know:

If you've been watching the banks lately, you'll have noticed interest rates ticking upward.

But what's actually happening behind the scenes tells a different story.

Over the last month or so, many of the banks have bumped their 1-year rate from around 4.49% to 4.59%.

But what people won't see is that most are discounting that rate back down to an average of 4.48%.

So the interest rate you see on bus backs and billboards has gone up. But most Kiwis aren’t paying any more on that rate.

We also see this with the 2-year rate. The average bank is discounting this rate by 0.16%.

It’s true. Rates have gone up. But if you just look at the advertised rates, you'd think they've gone up more than they actually have.

Banks are worried about the war in Iran. And they are seeing their costs go up.

But they're still competing hard for business. So they're discounting behind the scenes.

The sticker price goes up. But, some of the negotiated prices stay roughly the same.

That’s really hard to see from the outside.

Today, Iran and the United States agreed to a 2-week ceasefire. That’s already pushed the price of oil below US$100 a barrel.

That matters for New Zealand because oil prices feed directly into inflation.

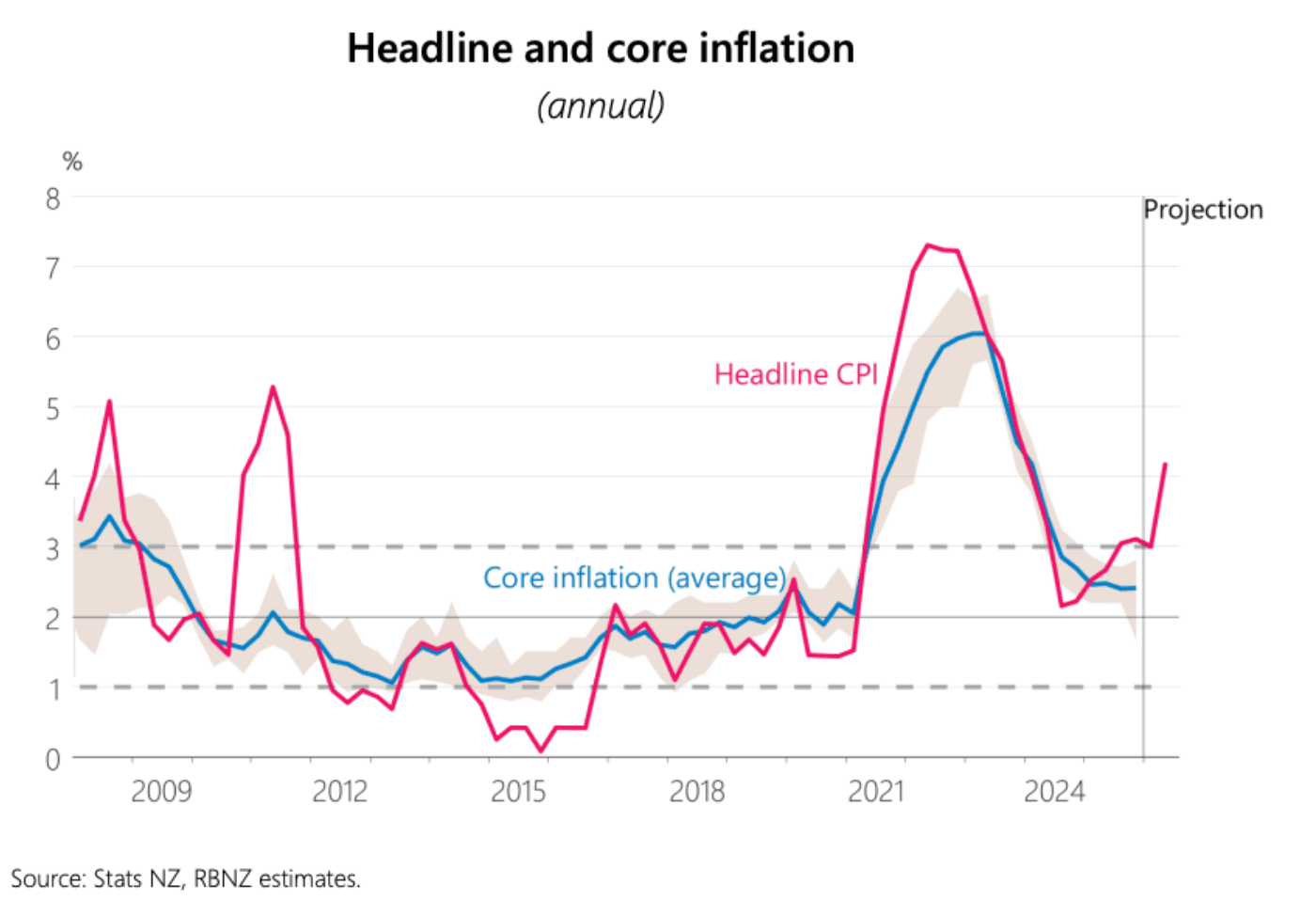

The Reserve Bank expects headline inflation to rise to 4.2% by June this year. (Just announced today). That's outside their 1–3% target band.

But in today’s speech, the Reserve Bank Governor, Dr Anna Breman, said that that number alone won't necessarily trigger an OCR increase.

What they're watching is core inflation – the underlying trend once you strip out the volatile stuff like fuel and food prices.

So if the ceasefire holds and oil prices stay low, inflation pressures ease. That takes pressure off the Reserve Bank to hike the OCR.

And mortgage rates stay where they are.

If the ceasefire falls apart and oil spikes again, we're looking at more inflation. That could force the Reserve Bank's hand. And mortgage rates would likely rise.

Mortgage broker for over 10 years, property investor and Managing Director at Opes Mortgages

Peter Norris, a certified mortgage adviser with 10+ years of experience, serves as the Managing Director at Opes Mortgages. Having facilitated over $1.2 billion in lending for 2000+ clients, Peter is a respected authority in property financing. He's a frequent writer for Informed Investor Magazine and Property Investor Magazine, while also being recognized as BNZ Mortgage Adviser of the Year in 2018 and listed among NZ Adviser's top advisers in 2022, showcasing his expertise.

This article is for your general information. It’s not financial advice. See here for details about our Financial Advice Provider Disclosure. So Opes isn’t telling you what to do with your own money.

We’ve made every effort to make sure the information is accurate. But we occasionally get the odd fact wrong. Make sure you do your own research or talk to a financial adviser before making any investment decisions.

You might like to use us or another financial adviser